.avif)

How to Export to India Without Mistakes: A Practical Guide for Export Departments

Did you know that exporting to India can open up a market of over 1.4 billion consumers for your business? In this practical guide, we will share the key steps, strategies, and help you navigate the six fundamental steps to ensure your export process is successful and free of unnecessary complications.

When we decided to explore how to export to India for the first time, we faced a labyrinth of regulations, documents, and requirements that seemed endless. In our case, we discovered that the requirements for exporting to India vary significantly depending on the type of product. For example, while some processed foods enter with relative ease, other products require multiple certifications and permits.

Furthermore, it is essential to understand what can be exported to India before initiating any operation. Not all products have free access to the Indian market, and restrictions can change frequently. Even for those considering exporting to India from Italy or other European countries, the procedures can be confusing if not well understood.

Step 1: Verify if your product can be exported to India

Before initiating any commercial operation with India, it is essential to verify if your product can legally enter this country. The Indian Customs Administration establishes different requirements according to the type of product, and not knowing them can result in costly delays or even the rejection of your goods.

Consult the ITC-HS classification

The first step to export to India is to correctly identify the ITC-HS (Indian Trade Clarification based on Harmonized System) code of your product. This eight-digit system is used by Indian customs to classify all goods intended for import and export.

To determine if you need a special license to export your product, you must first classify it according to this system. India uses the ITC-HS as the primary method to categorize articles in international trade operations. This code will allow you to know exactly which documents you will need and which tariffs will apply to your goods.

It is important to pay special attention to the product description and its HS code during the first shipment. Indian customs authorities use the first registration as a reference for future similar shipments. If by mistake your product ends up classified in a category with higher import rates, it will be practically impossible to modify it later.

Identify if it is restricted, canalized, or prohibited

Once the ITC-HS code is identified, you must verify in which category your product falls:

Freely importable products: Most products can be freely imported into India without specific restrictions, provided the importer has a valid Import and Export Code (IEC).

Restricted products: Require a special license issued by the competent Indian authorities. The validity of these licenses is 24 months for capital goods and 18 months for the rest. These include certain agricultural products, textiles, garments, specific pharmaceuticals, and some electronic products.

Canalized products: Can only be imported through specific procedures and through authorized agencies. They include petroleum derivatives, bulk agricultural products like grains or vegetable oils, and certain pharmaceutical products.

Prohibited products: Are completely prohibited in all import channels. They include wildlife and endangered species, antiques, cultural artifacts, certain hazardous chemicals, and counterfeit goods.

Verify if it requires sanitary or technical permits

In addition to the general classification, many products require specific technical or sanitary certifications to enter the Indian market:

For unprocessed products of plant origin, it is necessary to obtain an import permit granted by the "Plant Quarantine Organization India". The exception are certain products (mainly medicinal plants) included in Schedule VII of the "Plant Quarantine Order 2003", which only require a phytosanitary export certificate.

In all cases, even for Schedule VII products, the Indian phytosanitary authority must first conduct a pest risk analysis. This process can take several years. Subsequently, a protocol is signed detailing the diseases the products must be free from and additional requirements such as fumigation or special treatments.

For products of animal origin (meat, milk, eggs, etc.), a sanitary import permit is required. The Indian importer is responsible for processing this permit for each operation, and the goods must be accompanied by a veterinary certificate issued by the health authorities of the exporting country.

On the other hand, certain products such as milk and dairy, meats, fish, egg powder, infant food, and nutritional supplements require that the production facilities be previously authorized and registered by the Indian authorities.

It is advisable to work with an experienced Indian importer or customs agent, as Indian authorities occasionally implement new requirements that may be unknown to exporters without experience in this market.

Step 2: Obtain the IEC Code and comply with legal requirements

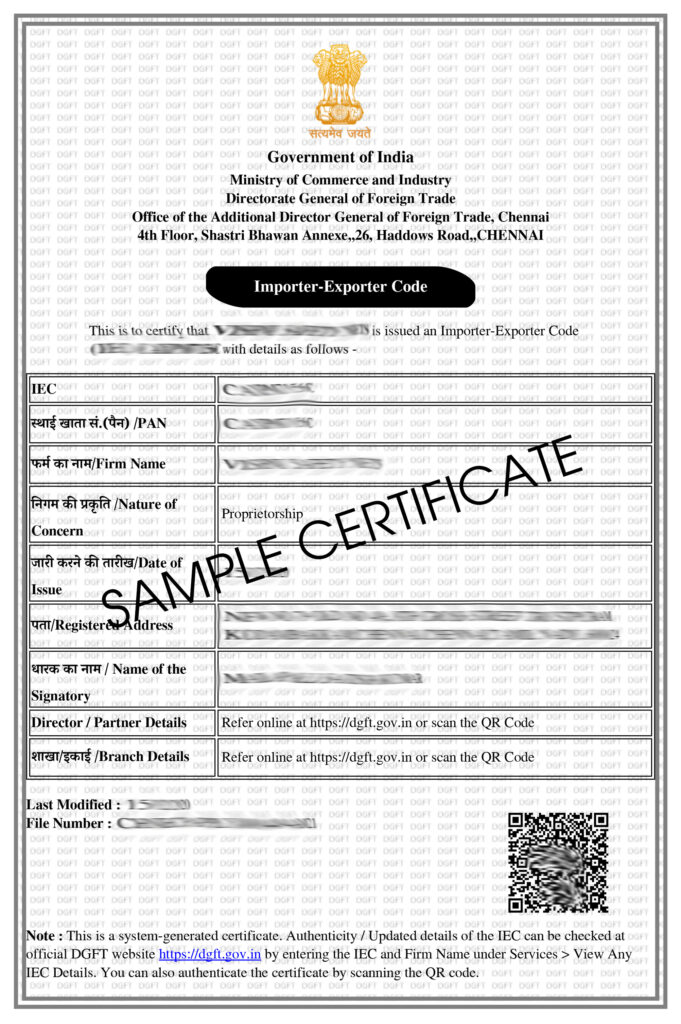

Once verified that your product can enter the Indian market, the next indispensable step to export to India is to obtain the Importer-Exporter Code (IEC). Without this document, no product will be able to cross Indian customs nor will you be able to make international payments legally.

What is the IEC and how to obtain it

The IEC Code (Importer-Exporter Code) is a unique 10-digit alphanumeric identifier issued by the Directorate General of Foreign Trade of India (DGFT). This code functions as the mandatory commercial identification for any company that wishes to perform import or export operations with India.

The IEC has permanent validity (for life) for your company, meaning it does not need renewal. However, it is mandatory to update or electronically confirm the IEC data every year between April and June, even if there are no changes.

To apply for the IEC code, you must follow these steps:

Visit the official DGFT website (Directorate General of Foreign Trade | Ministry of Commerce and Industry | Government of India ) and create an account

Navigate to "Services" > "IEC Profile Management" > "Apply for IEC"

Complete form ANF 2A with your company information

Upload the required documents (detailed in the next section)

Sign the application (via digital certificate or Aadhaar electronic signature)

Make the payment of 500 rupees (approximately €5.5)

Normally, if all documents are in order, you will receive your IEC code within 1 to 7 business days. In some cases, the DGFT may physically verify your company's address before issuing the code.

Documentation needed for registration

To complete your IEC application, you will need to prepare the following documents:

PAN tax identification: For sole proprietorships, the owner's PAN is required; for other entities, the company's PAN

Proof of business constitution: According to the type of company:

Sole Proprietorships: Owner's Aadhaar Card

Partnerships: Partnership deed

Limited Liability Partnerships (LLP): Certificate of incorporation issued by MCA

Private/Public companies: Certificate of incorporation issued by MCA

Trusts/HUF/Societies: Registration certificate

Proof of business address: Rental agreement, sale deed, recent utility bill (electricity, telephone) or Aadhaar Card

Proof of bank account: Cancelled cheque with the company name pre-printed or bank certificate confirming the name, account number, and IFSC code

Digital photograph: Passport size (3x3 cm) of the owner/manager/director signing the application

All documents must be clearly scanned and in PDF format, except the photograph, cancelled cheque, and PAN card, which must be in GIF format.

Common errors when registering the IEC

To avoid delays in obtaining your IEC code when exporting to India, you must avoid these frequent errors:

Inconsistent information: Ensure the company name on the application matches exactly the one on the PAN and banking documents

Incomplete or illegible documentation: Provide all required documents with good scanning quality

Incorrect business address: The address must be verifiable, as the DGFT may perform physical verifications before approving the application

Error in selecting the company type: Correctly select if you are a sole proprietorship, partnership, LLP, etc., as this affects documentary requirements

Lack of annual update: Although the IEC has permanent validity, not updating the data annually can result in the suspension of the code

Attempting to import without IEC: Many novice exporters mistakenly believe they can start operations while processing the IEC, but without this code the goods will not be able to cross Indian customs

On the other hand, if you do not wish to establish an office immediately in India, you can work with a local importer who already has an IEC code, but they must also be registered for the goods and services tax.

Step 3: Apply for necessary licenses and certificates

After obtaining the IEC code, the next challenge to export to India is to get the specific licenses and certificates that each type of product requires. This phase is crucial, as without these documents the goods could be held in customs, generating additional costs and significant delays.

Import and export licenses

For products restricted according to the ITC-HS classification, it is essential to obtain a specific license before carrying out any commercial operation. Indian customs authorities will not allow the entry of these articles without the corresponding license, which must explicitly detail the conditions and procedures to follow during export.

The validity period of these licenses varies according to the nature of the product:

24 months for capital goods

18 months for other merchandise

As for canalized products, these can only be imported through specific procedures and through authorized agencies. This category currently includes petroleum derivatives, bulk agricultural products (such as grains or vegetable oils), and some pharmaceutical products.

It is important to distinguish between general and specific licenses. General licenses allow importing goods from any country, while specific or individual licenses only authorize import from certain countries.

Sanitary and phytosanitary certificates

Products of plant and animal origin require additional certifications to enter the Indian market. For agricultural or primary horticultural products, a phytosanitary certificate issued by the Plant Quarantine Department of the exporting country is necessary, often with a fumigation endorsement.

For products of animal origin, the Indian importer must apply for a sanitary import permit issued by the Department of Animal Husbandry of the Government of India. This permit is a prerequisite for the goods to enter the country.

In the specific case of food, the Food Safety and Standards Authority of India (FSSAI) requires that importers obtain a specific license. This document is crucial for traceability and compliance with food safety regulations. Importers must apply for this license through the official Food Safety Compliance System (FoSCoS) website.

Certificates of origin and end-use

The certificate of origin is a document that verifies the country where the product has been produced, manufactured, or processed. This certificate establishes the provenance of the goods and is commonly required by customs authorities as part of the clearance process.

There are two main types of certificates of origin:

Non-preferential: Simply defines the origin of the goods without granting tariff benefits.

Preferential: Used for shipments between countries with trade agreements and demonstrates that the goods are eligible for reduced tariffs.

To obtain a certificate of origin, you can request it directly from the Chamber of Commerce of your country. You will need one for each shipment you make. In some countries it is possible to request this document online, while in others you must fill out a physical form and send it to your local chamber of commerce for stamping and approval.

On the other hand, the end-use certificate is a document by which the importer declares the intended use of the imported product. This certificate is particularly important for products that could have restricted or regulated uses, such as certain chemicals or dual-use technologies.

Remember that some countries require that an embassy or the Ministry of Foreign Affairs legally approve these certificates, which can delay the process. Therefore, it is advisable to initiate these procedures well in advance.

Step 4: Correctly prepare the export documentation

Accurate documentation constitutes the backbone of any successful export operation to India. Any error or omission in these documents can cause costly delays, fines, or even the total rejection of the goods at Indian customs.

Commercial invoice and packing list

The commercial invoice is an essential sales contract issued by the exporter to the importer. This document helps customs authorities determine the value of the goods to calculate taxes and duties. According to India's Foreign Trade Policy 2015-2020, this document is mandatory for all import and export activities.

For a commercial invoice to be accepted in India, it must include:

Detailed description of the goods

Unit and total value in an accepted currency (rupee, dollar, pound, or euro)

Delivery terms (Incoterms)

Complete and accurate information in English

Exporter and importer data that exactly matches KYC documentation

It is essential to avoid spelling errors or incorrect abbreviations, as even small discrepancies can cause significant delays.

On the other hand, the packing list provides specific details about the shipment's content. Although frequently presented together with the commercial invoice, it serves a different function: while the invoice focuses on commercial values, the packing list details the physical content.

This document must include:

Quantity and weight of each article

Number of packages

Type of packaging (pallets, boxes, containers)

Dimensions

Marks and identification numbers

Bill of Lading or Air Waybill

The Bill of Lading for sea shipments or the Air Waybill for air shipments are legally binding documents that certify that the goods have been shipped. These documents are essential for retrieving the goods at the destination and function as title to the cargo.

To correctly prepare a bill of lading, we must include:

Complete data of the exporter and consignee with addresses and contacts

Transport information (shipping line, vessel name, voyage number)

Details of the ports of origin and destination

Accurate description of the goods, including number of packages, type of packaging, weight, and dimensions

Freight costs and applicable surcharges

Unique tracking reference number

Signature and stamp of the carrier or their agent

In case of export by sea or air, we must present the "Shipping Bill", while for exports by road the "Export Report" must be presented.

Customs declaration and other forms

Once all necessary licenses are obtained, it is essential to present the import declaration in the prescribed Bill of Entry. This document provides information about the exact nature, quantity, and value of the goods entering the country.

If the goods are cleared through the Electronic Data Interchange (EDI) system, it is not necessary to present a formal declaration as it is automatically generated in the system. Nevertheless, we must send a cargo declaration with the required data.

Additionally, if we do not use the EDI system, it is mandatory to present supporting documents such as:

Certificate of origin

Inspection certificate

Bill of Exchange

Commercial invoice and packing list

In certain cases, we must also provide the Business Identification Number (BIN) from the Directorate General of Foreign Trade before completing the shipping bill.

For specific shipments, it may be necessary to present additional documentation, such as ARE-1 forms (central excise declaration) and GST invoices for tax compliance.

Step 5: Understand duties, taxes, and customs classification

The Indian tariff system may seem complex for those starting their export operations to this country. Understanding how taxes and duties are calculated is fundamental to avoiding unpleasant surprises that affect the profitability of your commercial operations.

How duties are calculated in India

India uses the CIF (Cost, Insurance, and Freight) method to calculate duties, meaning taxes are applied on the total value of the goods, including transport and insurance costs. The Indian tariff system is governed by the Customs Act of 1962 and applies ad valorem duties (percentage on value) ranging from 0% to 150%.

The Indian tariff structure includes several components:

Basic Customs Duty (BCD): The main tariff applied to all imported products, based on the HS code and origin of the product

Integrated Goods and Services Tax (IGST): Replaces previous taxes like CVD and SAD

Social Welfare Surcharge (SWS): An additional charge applied to customs duties

Antidumping and safeguard duties: Applied to specific products to protect the domestic industry

The average customs tariff in India is around 15%, although it is in the process of reduction according to WTO mandates. However, some products face significantly higher tariffs, such as alcoholic beverages, wines, and certain processed foods.

What is the IGST and how it is applied

The IGST (Integrated Goods and Services Tax) is part of the new GST system implemented in India. This tax replaces several previous levies such as the Countervailing Duty (CVD), the Special Additional Duty (SAD), and other fees that were previously applied to imports.

The IGST rates depend on the classification of the imported goods, as specified in the Lists notified under Section 5 of the IGST Act of 2017. The standard combined tax for goods imported into India is 28%.

There are exemptions from IGST for certain specific cases, such as goods imported by diplomatic missions, merchandise for display at specific events, products for research, and articles imported by passengers within certain limits.

Common errors in tariff classification

One of the most serious errors when exporting to India is the incorrect tariff classification of products. The World Trade Organization (WTO) has intervened in disputes over Indian tariffs, such as the case of technological products incorrectly taxed at rates of up to 20%.

Other frequent errors include:

Declaring a value lower than the real one to avoid taxes, which constitutes tax evasion and can result in sanctions

Confusing the HS classification, which can lead to paying higher duties than necessary

Not knowing about trade agreements that could provide preferential tariffs

Not verifying if the product is subject to antidumping measures, which can raise the tariff up to 48%

Step 6: Use digital tools and avoid logistical errors

The successful implementation of digital tools is the last link to guarantee that our exports to India arrive without problems. These platforms have transformed international trade, reducing paperwork and streamlining processes.

How to use the ICEGATE and CIP portal

ICEGATE (Indian Customs Electronic Data Interchange Gateway) is the central platform for connecting exporters with Indian customs. After registering on its official site, we can access essential services such as:

E-filing of customs documentation

Electronic payment of duties and taxes

Real-time shipment tracking

On the other hand, the Indian Customs Compliance Portal (CIP) allows us to consult specific requirements for any of the 12,000 available tariff headings. We only need to enter the CTH code of our product to obtain detailed information on procedures, documentation, and regulatory requirements.

Shipment tracking and customs clearance

To supervise our shipments to India, we can use different methods depending on the carrier. With India Post, tracking is done through:

Its official website with the "Track & Trace" function

SMS messages by sending "PISTA POST" to 166 or 51969

The Postinfo mobile application

The usual format of tracking codes consists of 13 characters (two letters, nine digits, two letters), such as EE123456789IN.

Frequent errors in transport and delivery

Among the most common failures are the incorrect choice of the CIP Incoterm (Carriage and Insurance Paid), which requires a comprehensive type A insurance according to Incoterms 2020. Many exporters are unaware of this update and contract only the minimum type C coverage.

Furthermore, it is common not to verify if the destination country requires that insurance coverage be contracted within its borders, generating legal problems. To avoid these situations, we must familiarize ourselves with India's specific regulations before initiating any commercial operation.

Conclusion

Exporting to India represents an extraordinary commercial opportunity for any company willing to invest time in understanding its regulatory processes. After meticulously following the six steps described, you will notice that the initial barriers begin to disappear, allowing access to a market of 1.4 billion potential consumers.

The prior verification of the export feasibility of your product undoubtedly constitutes the foundation of the entire process. This simple action will avoid costly rejections and unnecessary delays. Likewise, obtaining the IEC code establishes the legitimacy of your commercial operation before the Indian authorities.

The specific licenses and certificates function as keys that open doors in this market. Although they may seem like obstacles, these documents actually protect both consumers and exporters. Accurate documentation, on the other hand, is crucial to avoiding setbacks during customs clearance.

Certainly, understanding the Indian tariff system and the effective use of digital tools complete the preparation cycle. Many companies fail precisely by underestimating these last steps, considering them mere administrative procedures when they actually determine the final profitability of the operation.

The errors we used to make when exporting to India have now become valuable lessons we share with you. The difference between a failed export and a successful one lies mainly in exhaustive preparation and specific knowledge of the market.

Trade with India may seem complex initially, however, once the correct procedures are established, operations become more fluid and predictable. Our final advice: dedicate sufficient time to prepare each step described in this guide before starting your first export.

India awaits your products. Are you prepared to conquer one of the world's most promising markets?

Download the ranking of the main US importers by sector

Other articles

Join our newsletter

Market intelligence software for exporting enterprises.